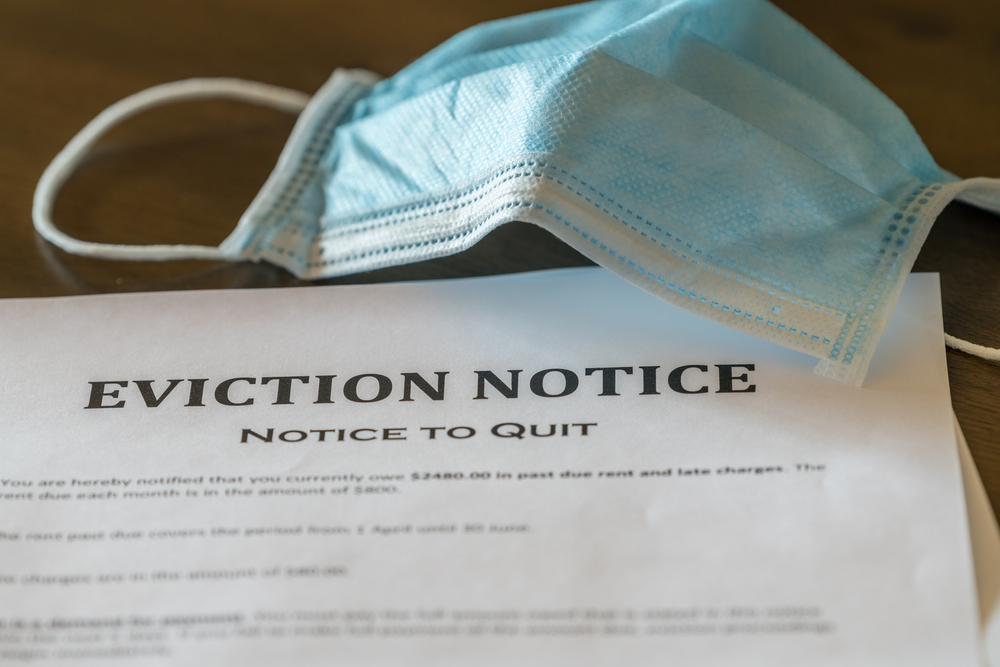

Courts throughout the country are inundated with eviction cases resulting from the economic impact of the coronavirus, while cities, states and the federal government have rushed to aid households with only mixed results.

A 120-day eviction moratorium mandated by the Congressional CARES Act expired on July 24. Meanwhile, some state-imposed eviction moratorium programs have similarly expired.

On Sept. 1, the federal Center for Disease Control and Prevention issued an order to temporarily halt housing evictions through Dec. 31 to prevent the spread of COVID-19.

These efforts often fail to cover many renters who have lost income and jobs because of the economic downturn caused by the coronavirus.

Evictions continue and thousands of families face homelessness.

RELATED: CARES act fraud not easy to define

RELATED: Mask exemptions are a rarity in the law

Since the COVID-19 pandemic began earlier this year, landlords have filed for nearly 54,000 evictions, according to The Eviction Lab at Princeton University, which has researched evictions since 2000 in nearly 30,000 communities.

As of the end of September, the cities most impacted by evictions during the pandemic include Houston, (11,940), Phoenix (10,898), Milwaukee (4,631), Cincinnati (3,132), Jacksonville (2,143) and Pittsburgh (1,055), according to The Eviction Lab.

According to the CDC there are about 30-40 million renters in the U.S. who are at risk of eviction: “A wave of evictions on that scale would be unprecedented in modern times.”

To put this in perspective, before Covid-19, less than a million renters were evicted each year.

Federal and state eviction bans don’t protect everyone

The current eviction crisis is not new and is growing.

“In America, families have watched their incomes stagnate, or even fall, while their housing costs have soared. Median rent has increased by more than 70% since 1995,” says Matthew Desmond, author of the Pulitzer-prize winning book Evicted: Poverty and Profit in the American City. He’s a professor of sociology at Princeton University, and chief investigator at Princeton’s The Eviction Lab.

“Meanwhile, only one in four families who qualify for housing assistance receive it, and in the nation’s biggest cities the waiting list for public housing is not counted in years but decades. The typical poor American family does not live in public housing but receives no government assistance whatsoever. The result? Today, the majority of poor renting families in America spend more than half of their income on housing, and at least one in four dedicates more than 70% to paying the rent and keeping the lights on,” Desmond wrote in a 2017 excerpt published in The Guardian.

As this trend was exacerbated by the COVID-19 economic downturn, the CDC’s effort to ease the housing crisis proclaimed the risk of infection for people forced into homeless shelters: “housing stability helps protect public health. …. Unsheltered homelessness also increases the risk that individuals will experience severe illness from COVID-19.”

The order, which carries a penalty of up to $250,000, bars landlords from pursuing evictions in areas not already protected by similar state or local eviction moratoriums.

While it allows local authorities to impose more restrictive bans, some states are cancelling their eviction bans. For example, Florida Governor Ron DeSantis recently cancelled his state’s moratorium on evictions and foreclosures to “avoid confusion” over potentially clashing rules with a federal ban on some evictions.

The CDC order is being challenged in federal court. A Virginia landlord claims “significant economic damages” and, in a joint lawsuit with other landlords and the National Apartment Association, is seeking to have the CDC order invalidated.

And even if the CDC order prevails, not every household will be protected. According to The Eviction Lab, hundreds of new evictions were filed in the weeks following the CDC eviction ban.

Also, temporary orders against evictions do not erase the obligation of tenants to eventually pay back all rent due. Such orders also often do not protect against the levying of fees, penalties or interest for nonpayment.

Who is protected against evictions?

Most eviction moratorium orders, whether federal or local, require all adults listed on a lease or mortgage to sign declarations that they have lost income due to the coronavirus. Importantly, any evictions or foreclosures initiated for reasons other than paying rent or mortgages are allowed to go forward.

The CDC order also limits individual applicants’ 2020 income to $99,000 or less or $198,000 for joint tax filers. Applicants who were not required to report income to the IRS or who received CARES Act stimulus checks are covered by the CDC order.

However, even if you have faithfully paid your rent, you still can be evicted if your landlord’s property is foreclosed by their bank, an action that legally ends your lease. The bank or new owner, if the property is sold, therefore has the right to evict any tenants.

Vague wording in the CDC order appears to exempt mortgage holders or temporary or seasonal tenants from the eviction moratorium. The order also allows foreclosures to proceed, but does not directly address post-foreclosure evictions.

The required declaration asserts under penalty of perjury that the applicant cannot make a housing payment because of a substantial loss of income, lost work hours or wages, a layoff, or “extraordinary” (more than 7.5 percent of adjusted annual income) out-of-pocket medical expenses.

Under the eviction moratorium, applicants are expected to use their “best efforts” to make partial rental payments.

It’s important to note that the commercial sector is not directly protected against evictions by the CDC order. Some states did impose temporary moratoriums on commercial-real-estate evictions, but most have expired.

Federal loans under the CARES Act may have helped some businesses, but that money has largely run out. Many businesses, particularly in the hospitality sector, have permanently shut their doors, leaving commercial landlords without income.

What to do if you get an eviction or foreclosure notice

If you are a renter affected financially by the coronavirus and facing eviction, be sure that every adult on your housing lease completes the CDC declaration form before sending it to your landlord.

Some local governments are offering financial assistance for renters and homeowners unable to pay their housing bills. For example, Hillsborough County in Florida has instituted a Rapid Recovery Assistance Program that offers help in paying rent, mortgages and utility bills.

Also, be sure you have not violated any of your housing lease or complex rules, since such violations are not covered by the eviction moratorium.

If you are a homeowner, there is no similar blanket protection for non-payment of mortgages. State rules differ widely. However, If you have a federally-backed mortgage you may be protected through the rest of 2020.

The CARES Act, which has now expired, prohibited lenders and mortgage servicers from beginning foreclosure proceedings on mortgages backed or held by the FHA, the VA, the USDA, Fannie-Mae or Freddie Mac. This protection extends through Dec. 31, 2020.

If you have a standard, non-governmentally-backed mortgage, your bank may have a forbearance program in place that would allow you to suspend or reduce your payments for a certain period of time.

Also, according to the National Consumer Law Center, state orders barring foreclosure evictions often do not stop foreclosure proceedings or post-foreclosure property sales. Under federal law, mortgage holders cannot initiate foreclosures for at least 120 days after the homeowner becomes delinquent on their mortgage. But there can be exceptions and state laws may differ in how they regulate foreclosures and evictions.

As of mid-September, CNBC reported that about 3.7 million mortgage borrowers, or about seven percent of all active mortgages, had arranged mortgage forbearance with their lenders. Seriously delinquent mortgages had more than doubled by June, the highest level in five years.

The federal Consumer Financial Protection Bureau has published guidelines to help you negotiate a mortgage forbearance for your home.

But understand that whether you are a renter or a mortgage-holder, those unpaid debts do not disappear and you will be required to repay them, plus interest and fees, eventually. Depending on the type of debt and your legal jurisdiction, you may be required to pay the debt in full or you may be able to amortize it over time.

In the case of evictions, landlords are required to officially notify a tenant. The timing of that notice and the subsequent eviction process differs from state to state. If you decide to fight the eviction, your case will likely end up in court. And if you lose, a law enforcement officer may show up at your door.