As Virginia personal injury lawyers, we know there are concerns about how the shutdown could impact claims. A key issue is the effect it has on TRICARE and Medicare liens.

The economy touches nearly every part of daily life, including the legal system. In Tampa Bay, shifts in the economy can directly influence personal injury claims and how they are

The University of Wisconsin, along with its NIL collective VC Connect, filed a groundbreaking lawsuit against the University of Miami, alleging interference with binding NIL contracts and illegal tampering. The

On March 12, President Biden signed a $1.9 trillion COVID-19 relief bill into law. This relief bill comes a year after the COVID-19 virus forced states into various stages

Good news for law school graduates and others in the legal profession. A year after the earliest Covid-19 cases hit the United States prompting a near-shutdown of the economy, there

While people across the country struggled to pay their bills and lined up at food banks to feed their families, authorities say, some crooks struck it rich and took advantage

Millions of Americans are unemployed, and thousands of businesses are struggling amid a crushing recession brought about by the COVID-19 pandemic. Yet bankruptcy filings remain at historic lows.

The number

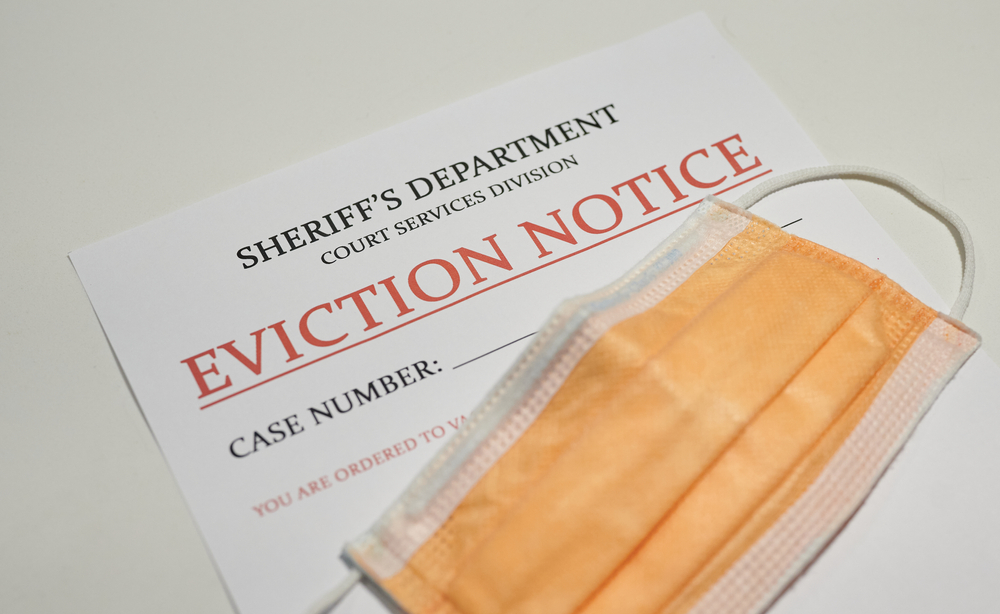

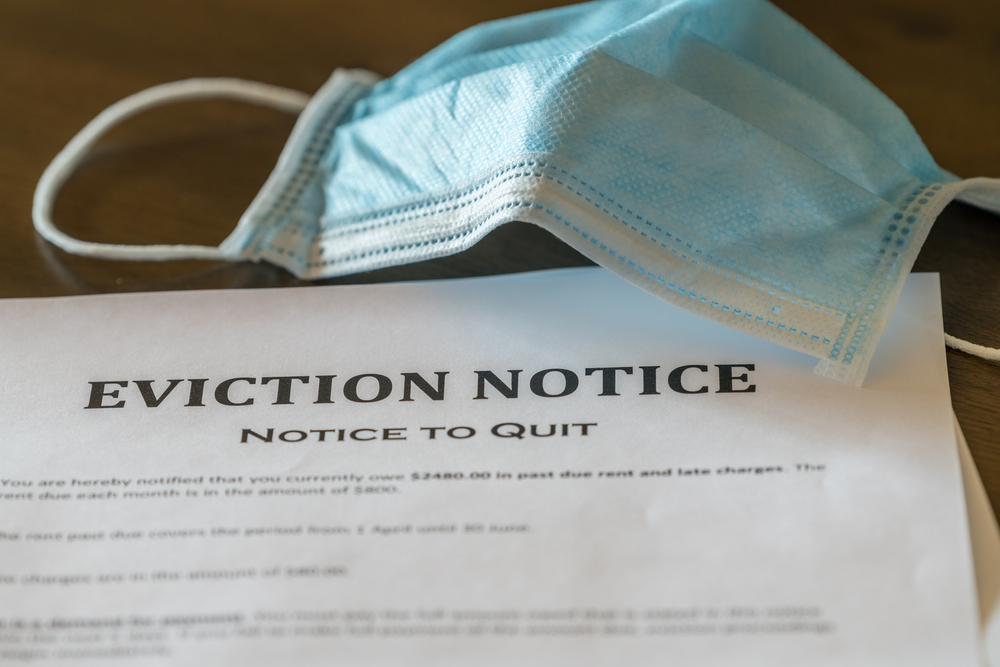

A new free tool designed by Suffolk University’s law school is helping thousands of people stave off eviction while the country remains in the grips of COVID-19.

Centers for

Courts throughout the country are inundated with eviction cases resulting from the economic impact of the coronavirus, while cities, states and the federal government have rushed to aid households with

A new report from the Brennan Center for Justice at NYU School of Law reveals exposure to the criminal justice system, no matter the length of time, carries consequences that

While Congress is working to root out CARES Act fraud connected to billions in business loans awarded during the COVID-19 crisis, small business owners are concerned about whether they followed the rules or will face the feds’ wrath if they didn’t.